Notice of 2025 Annual Meeting and Proxy Statement

Go to Home

Open index

Search

Index

Front Cover

Letter from Chair, President & CEO

Letter from Independent Directors

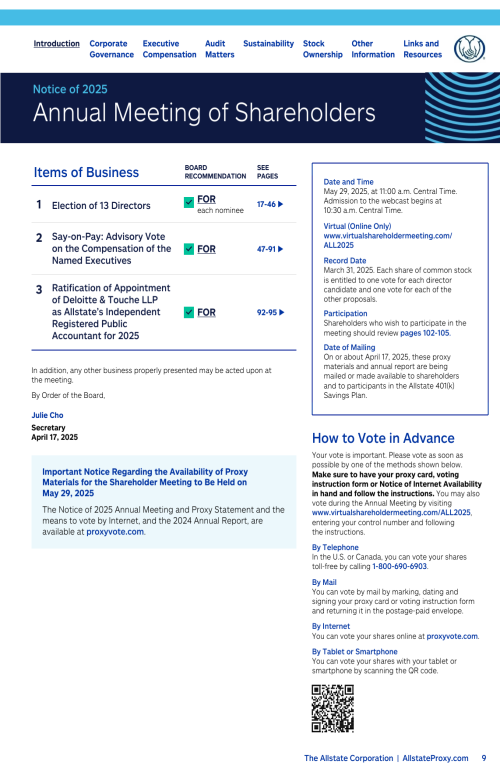

Notice of 2025 Annual Meeting of Shareholders

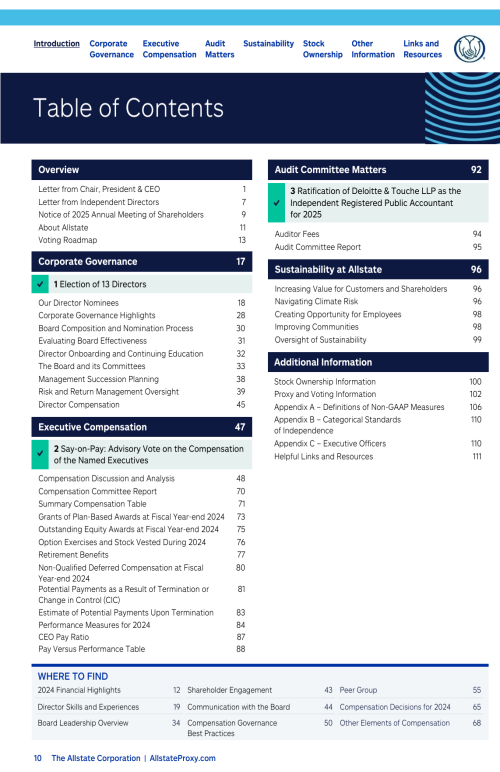

Table of Contents

About Allstate

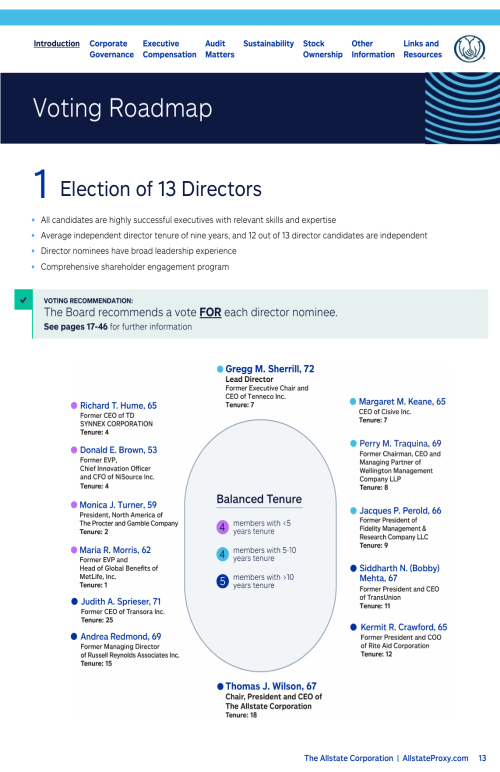

Voting Roadmap

Corporate Governance

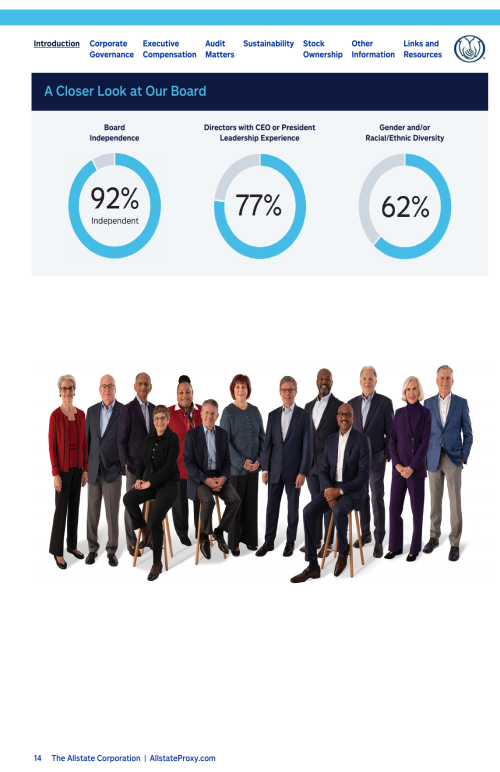

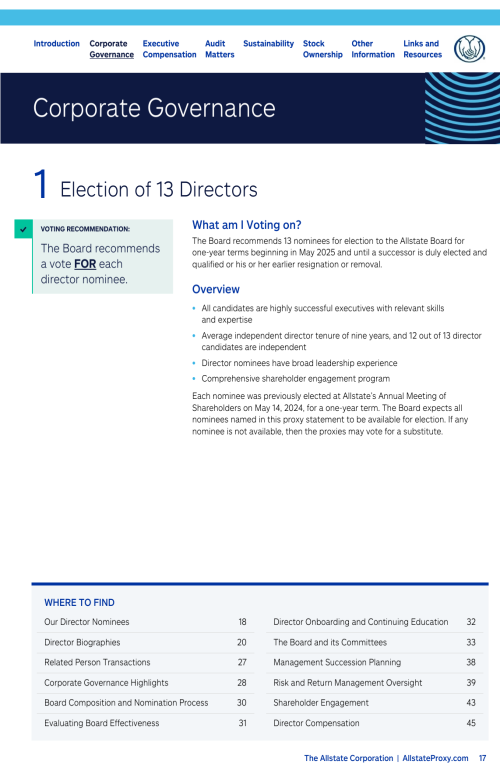

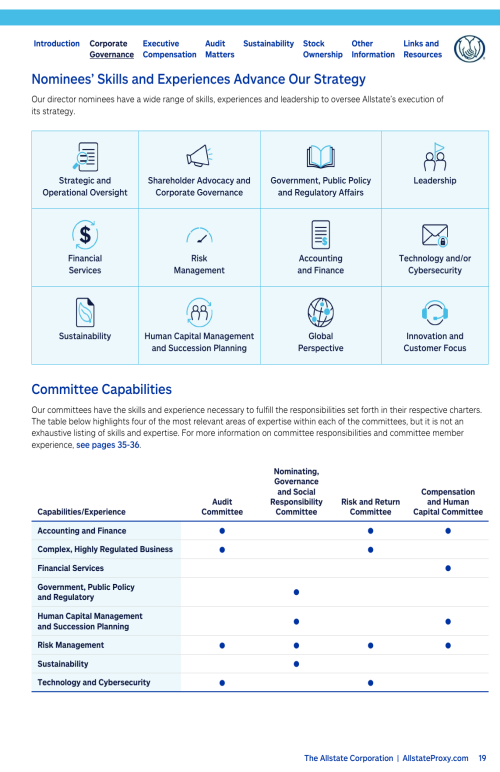

Proposal 1 Election of 13 Directors

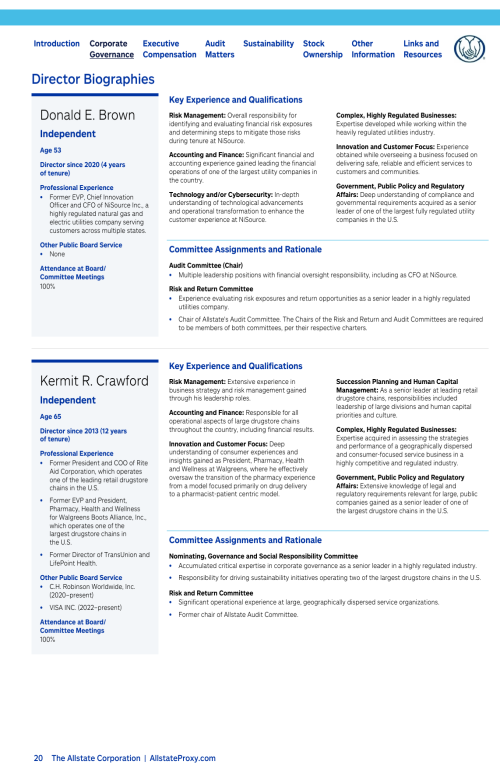

Our Director Nominees

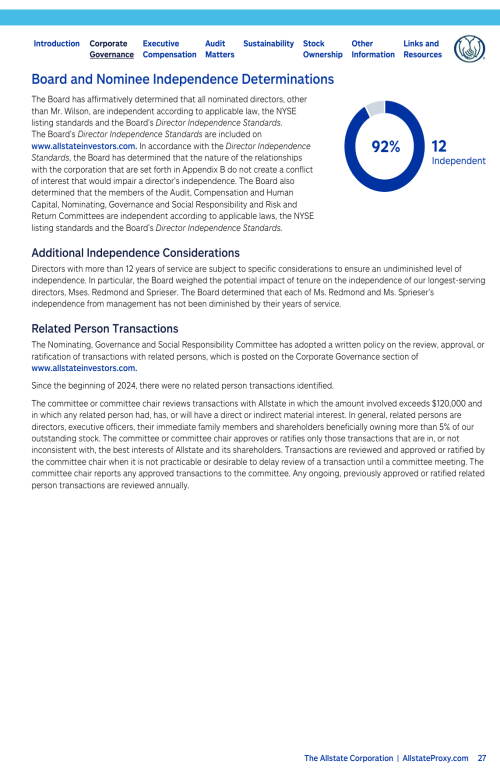

Corporate Governance Highlights

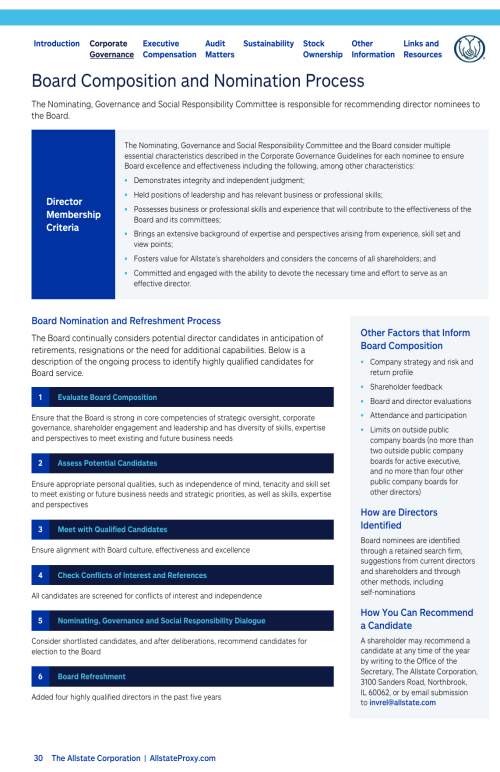

Board Composition and Nomination Process

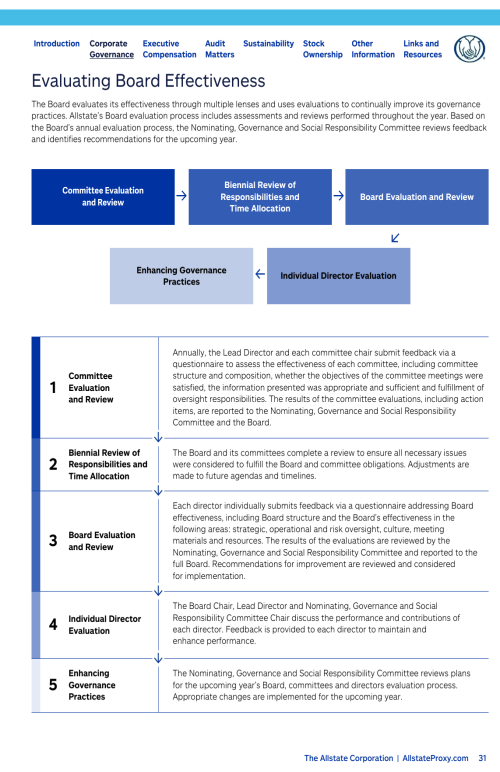

Evaluating Board Effectiveness

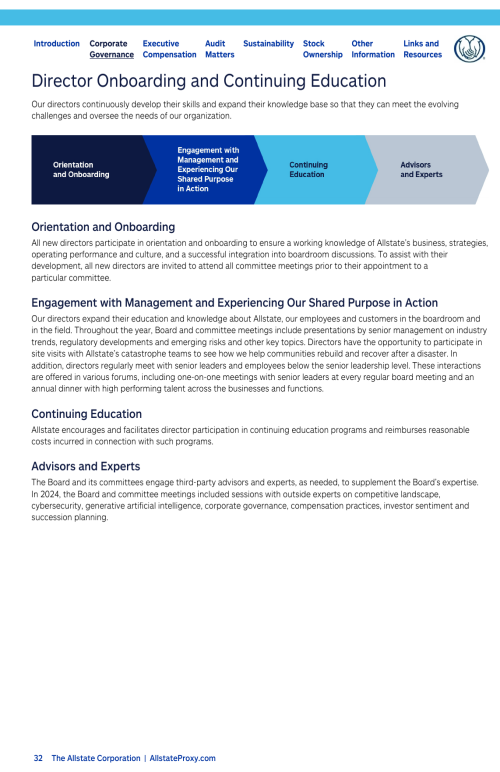

Director Onboarding and Continuing Education

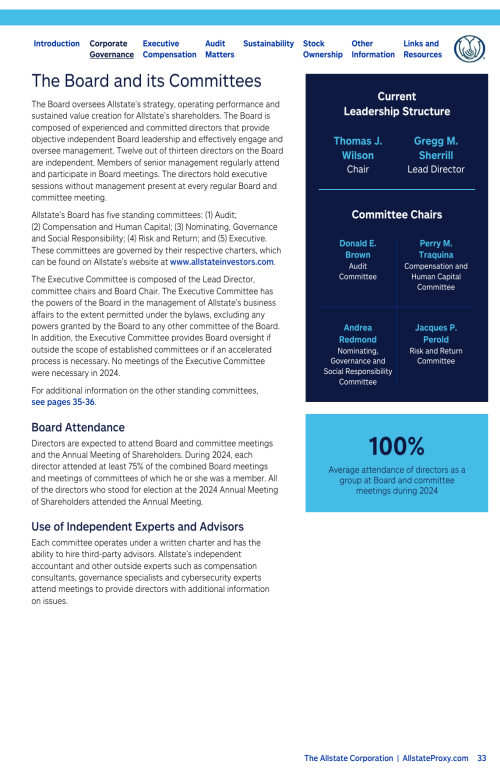

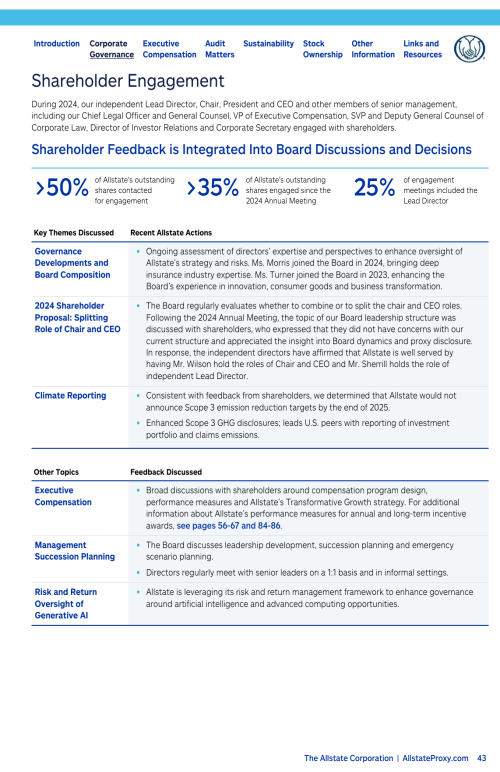

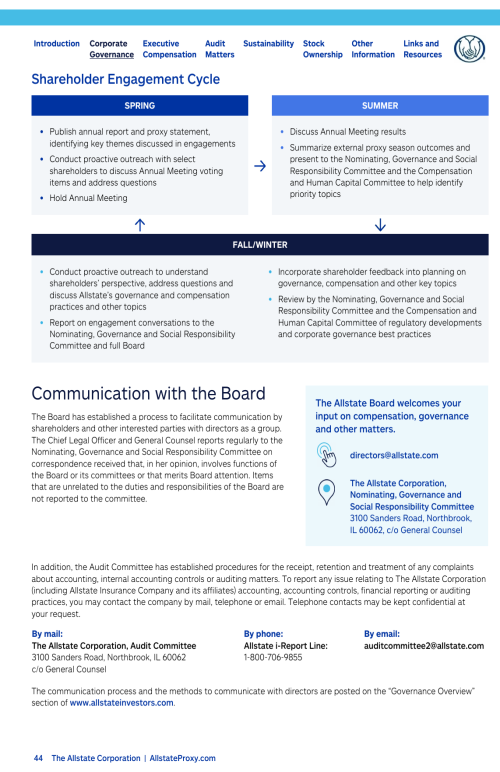

The Board and its Committees

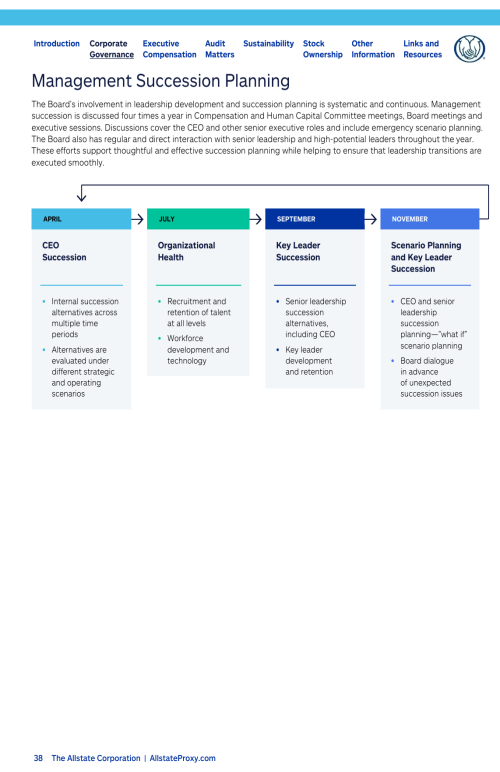

Management Succession Planning

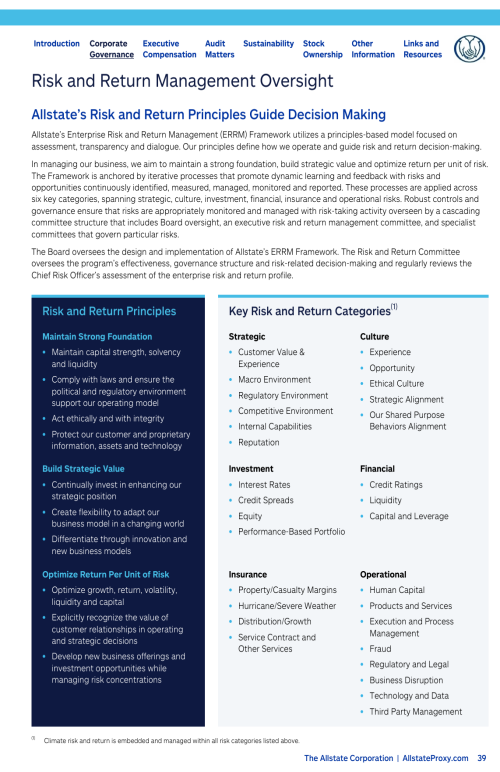

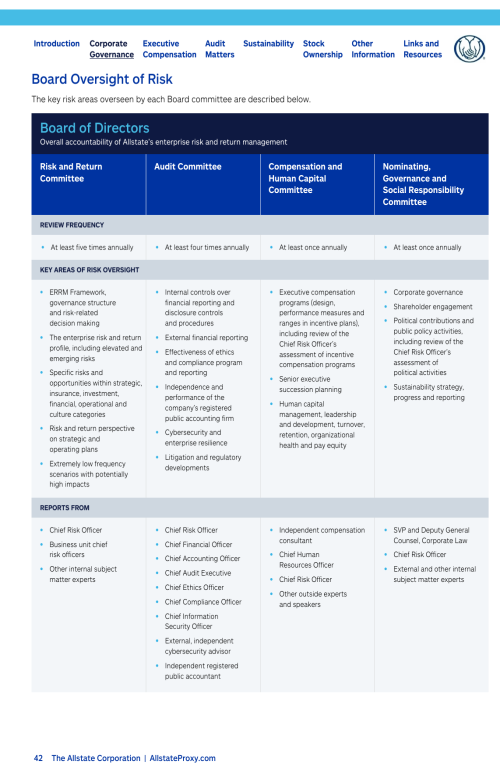

Risk and Return Management Oversight

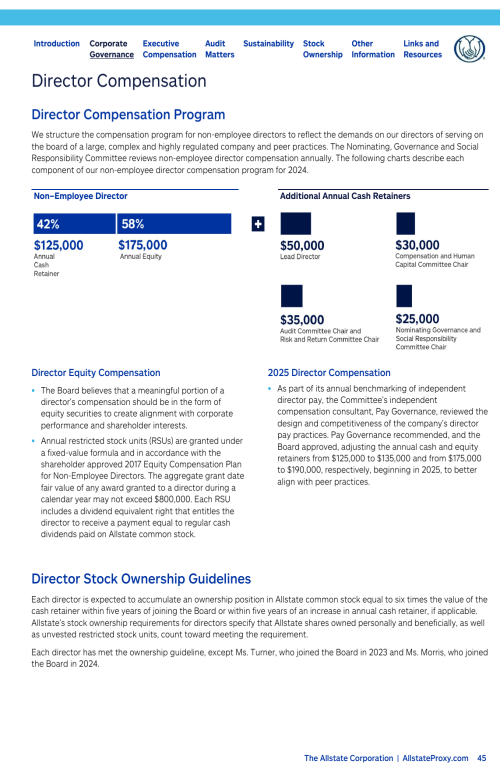

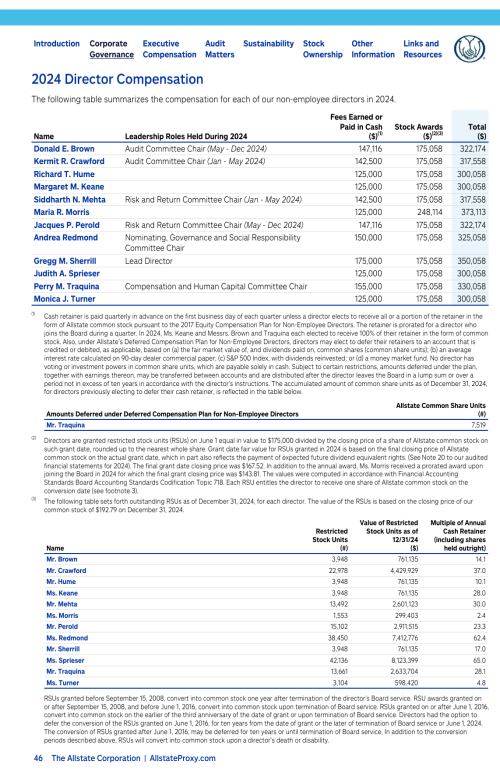

Director Compensation

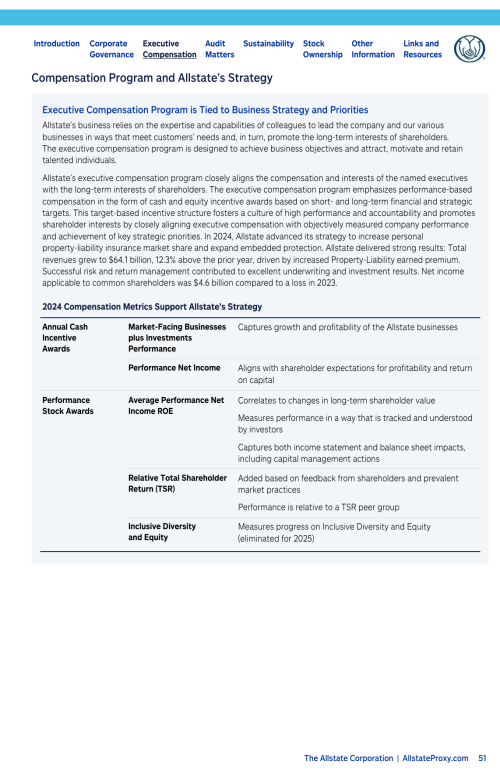

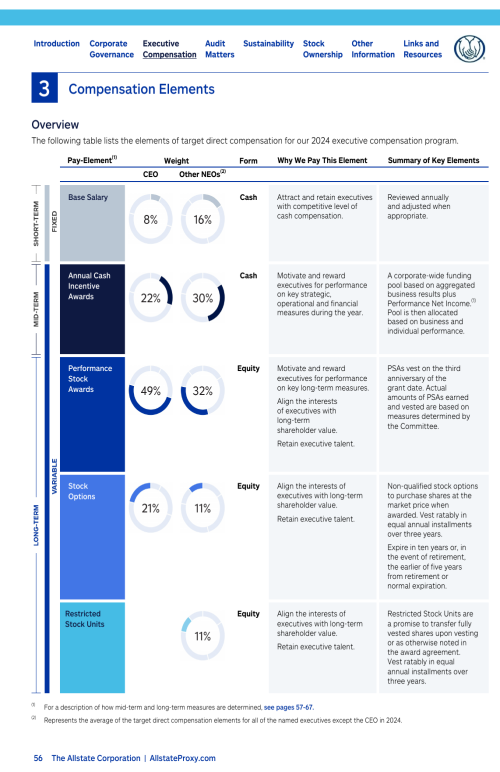

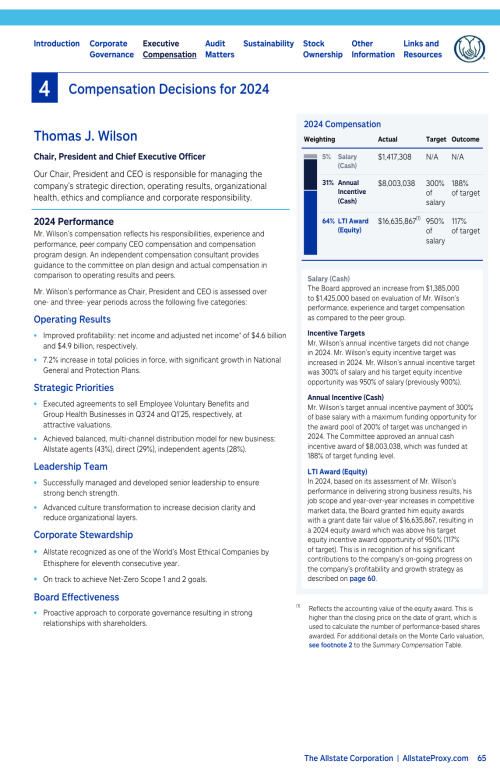

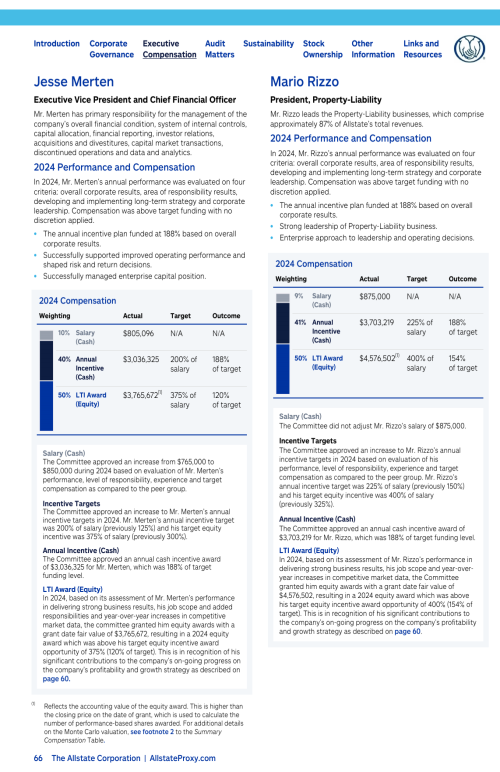

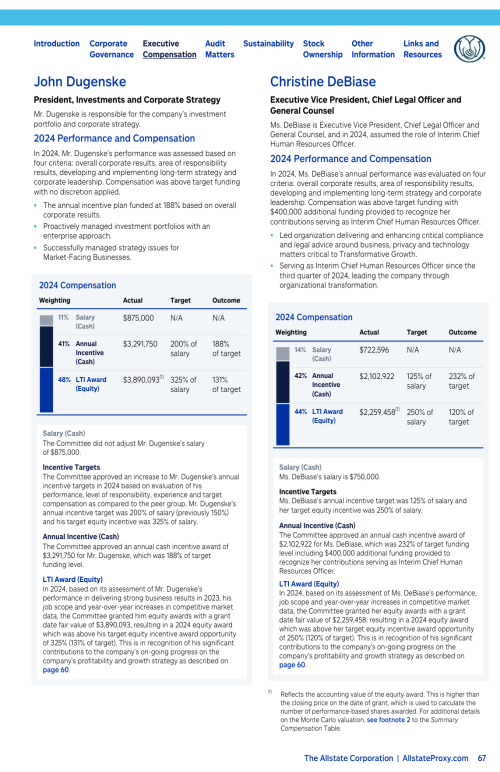

Executive Compensation

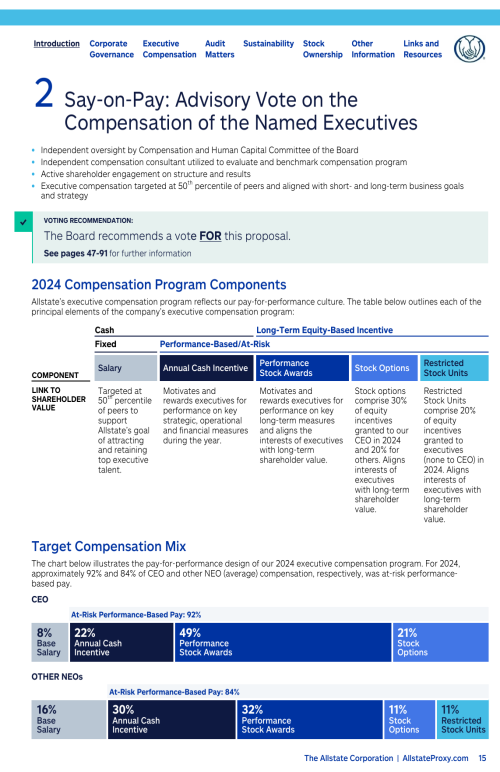

Proposal 2 Say-on-Pay: Advisory Vote on the Compensation of the Named Executives

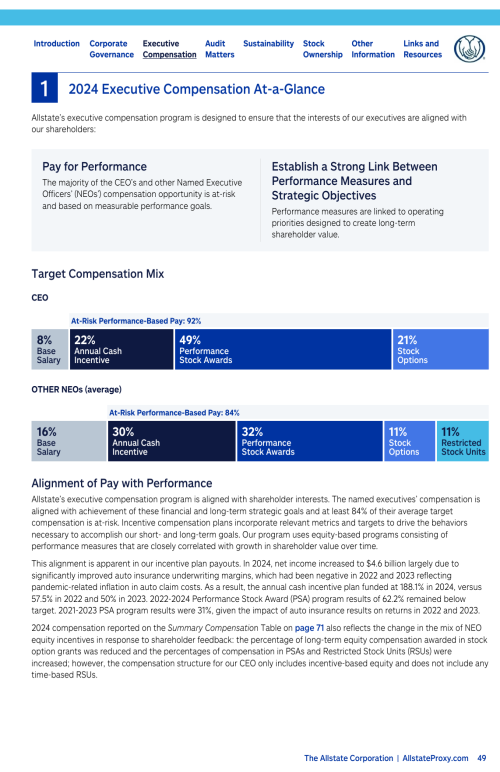

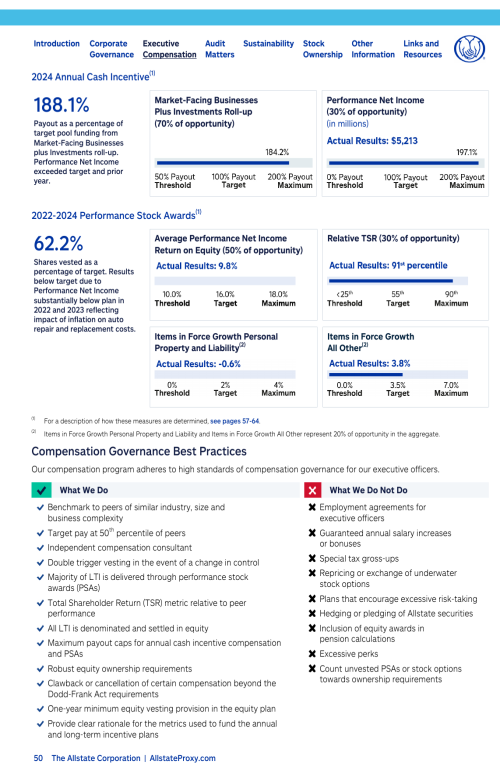

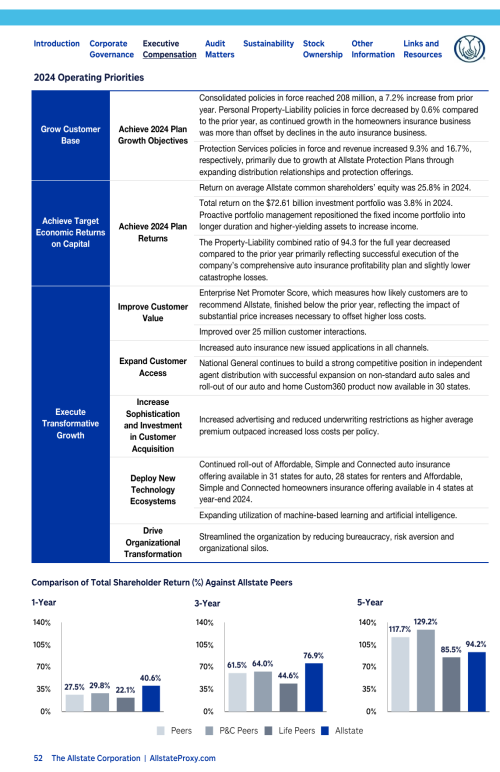

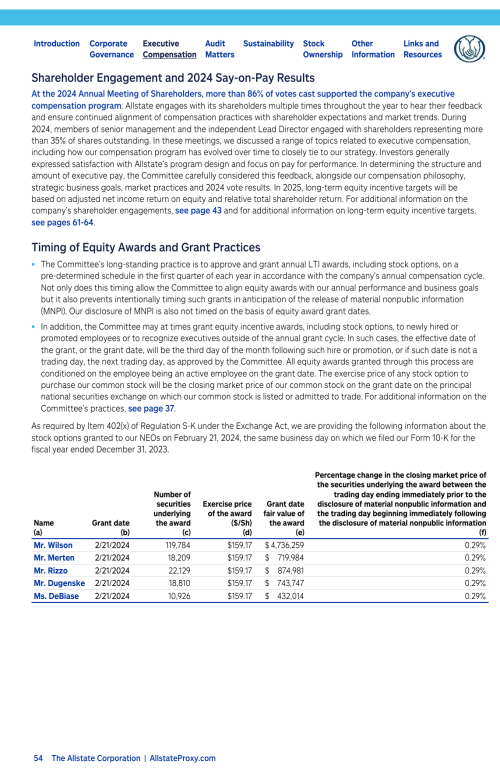

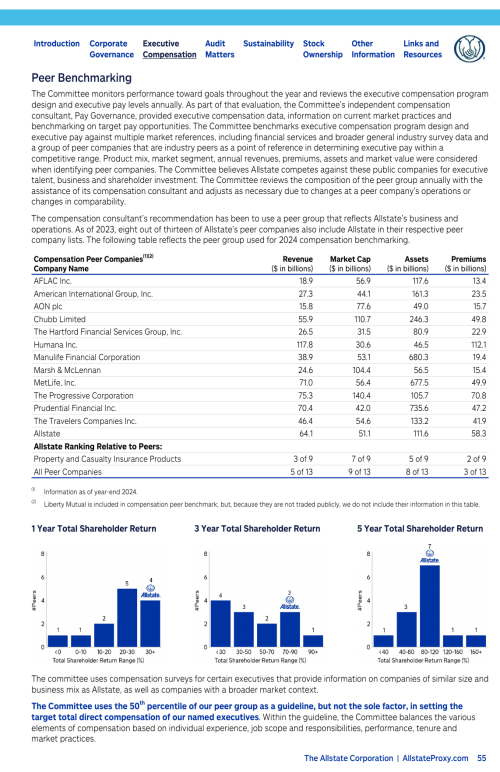

Compensation Discussion and Analysis

Compensation Committee Report

Summary Compensation Table

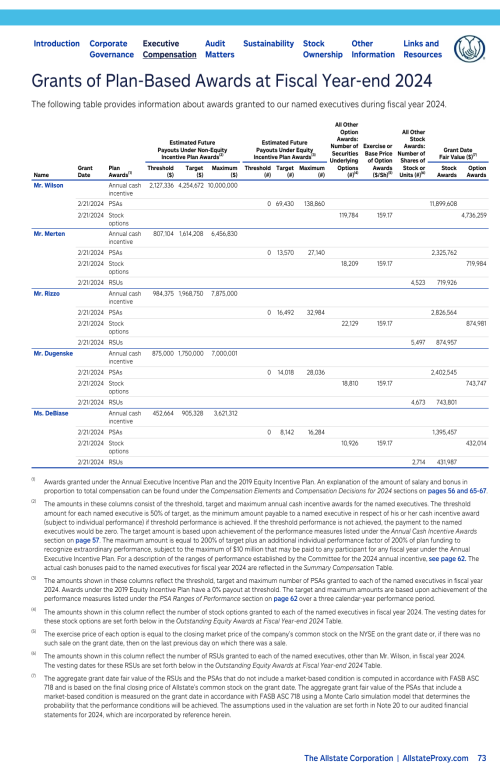

Grants of Plan-Based Awards at Fiscal Year-end 2024

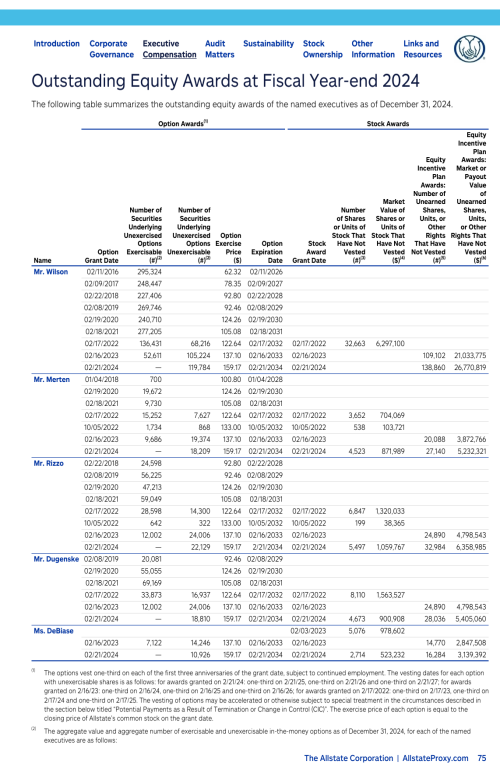

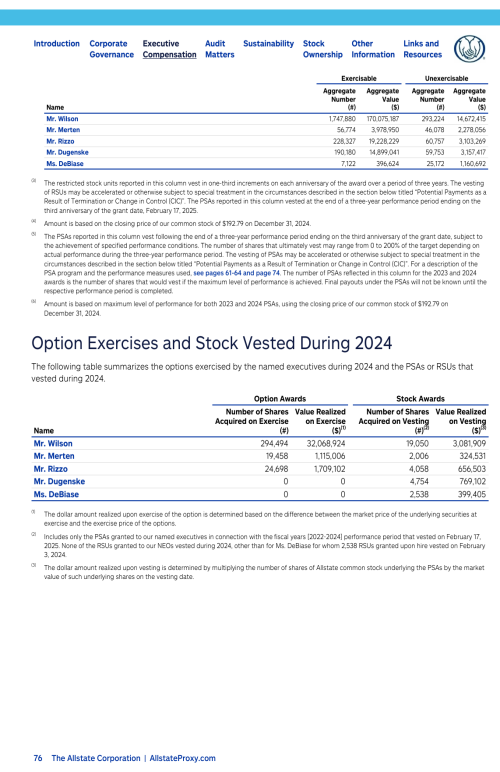

Outstanding Equity Awards at Fiscal Year-end 2024

Option Exercises and Stock Vested During 2024

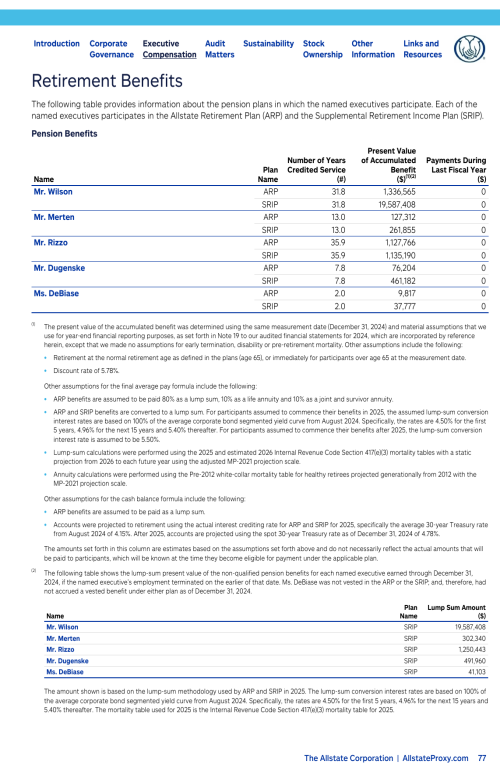

Retirement Benefits

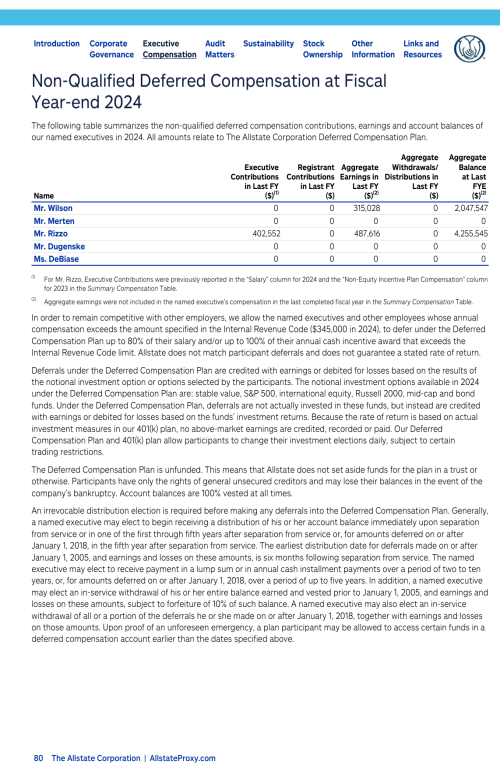

Non-Qualified Deferred Compensation at Fiscal Year-end 2024

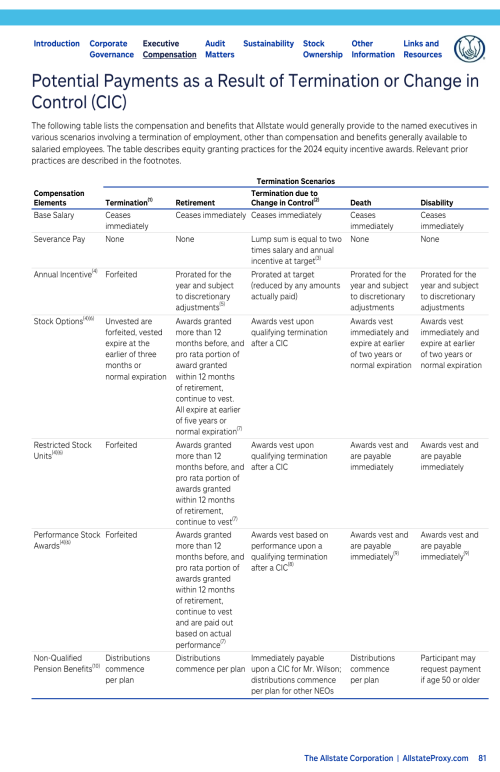

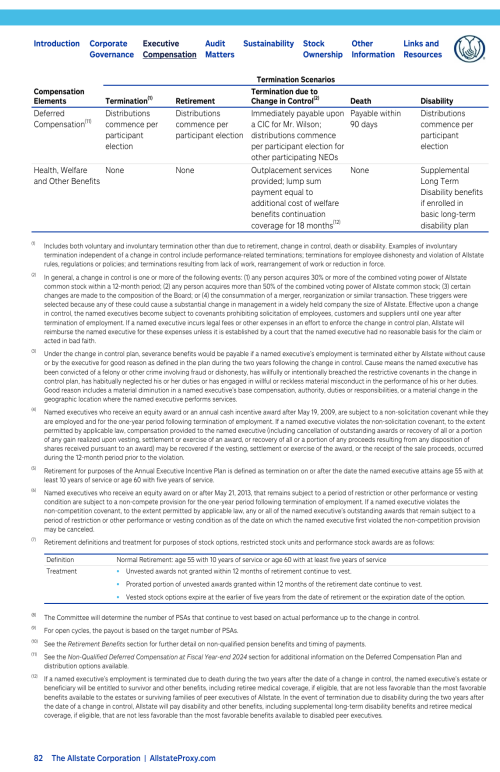

Potential Payments as a Result of Termination or Change in Control (CIC)

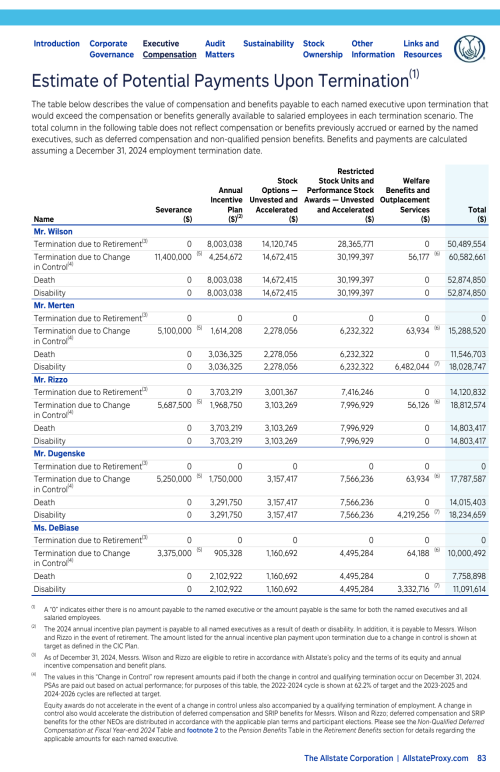

Estimate of Potential Payments Upon Termination

CEO Pay Ratio

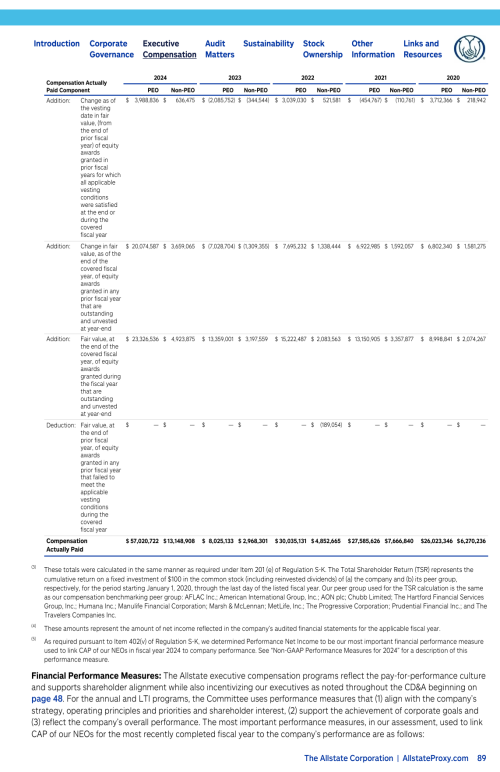

Pay Versus Performance Table

Audit Committee Matters

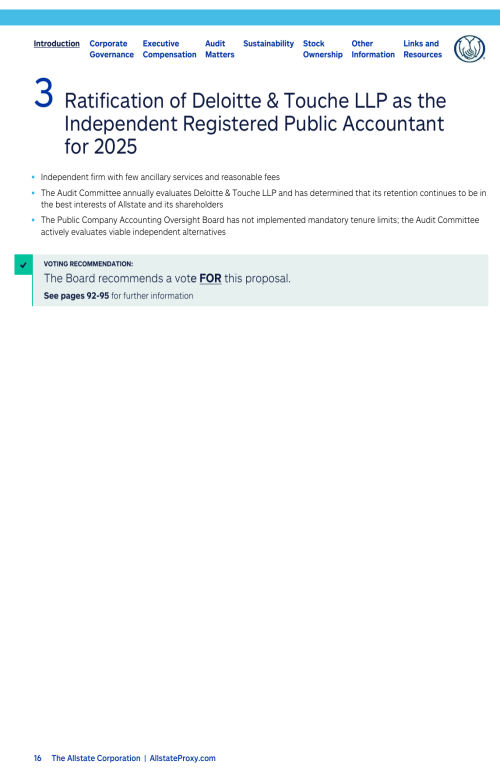

Proposal 3 Ratification of Deloitte & Touche LLP as the Independent Registered Public Accountant for 2025

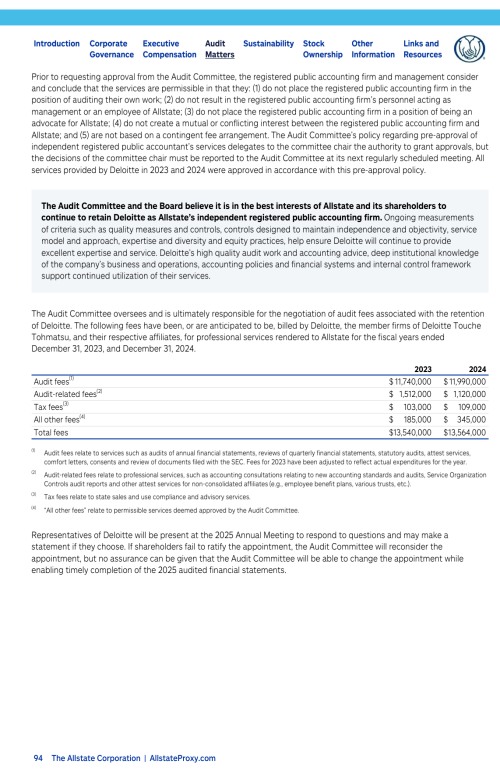

Auditor Fees

Audit Committee Report

Sustainability at Allstate

Increasing Value for Customers and Shareholders

Navigating Climate Risk

Creating Opportunity for Employees

Improving Communities

Oversight of Sustainability

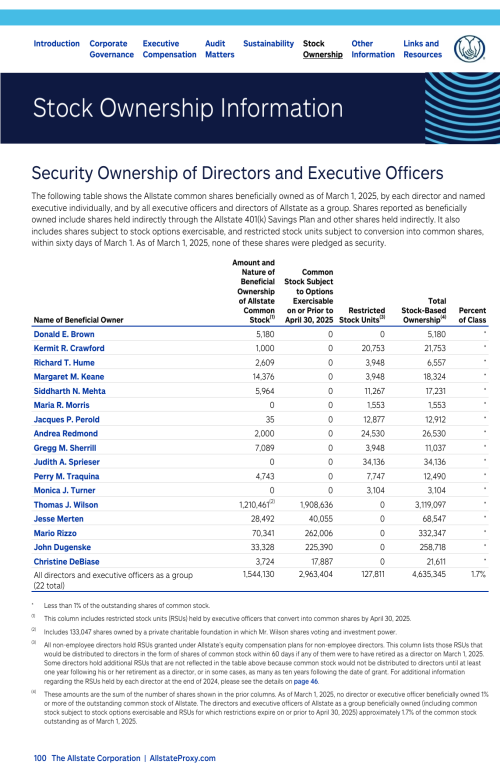

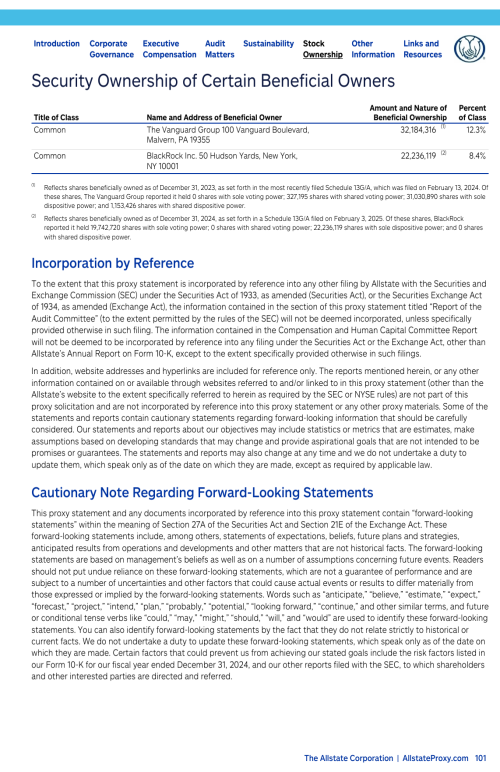

Stock Ownership Information

Proxy and Voting Information

Appendix A – Definitions of Non-GAAP Measures

Appendix B – Categorical Standards of Independence

Appendix C – Executive Officers

Helpful Links and Resources

Table of Contents 10K

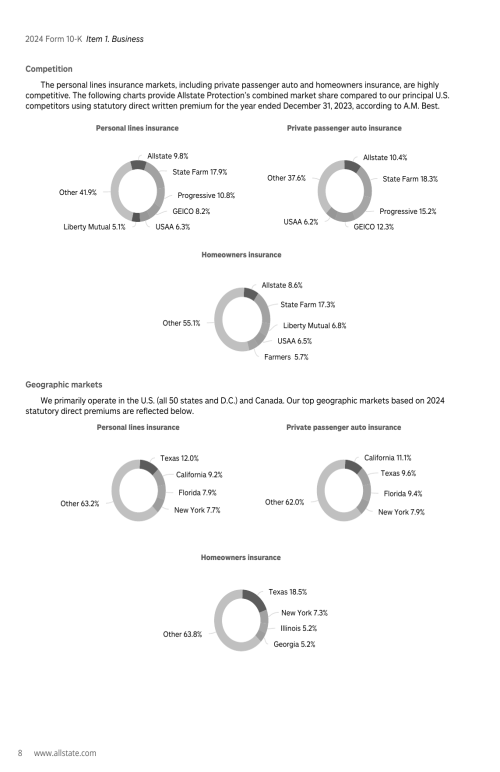

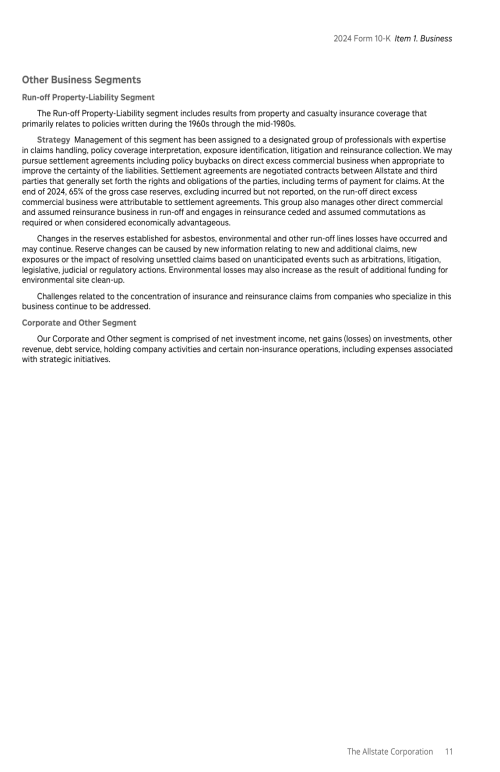

Item 1. Business

Overview

Strategy and Segment Information

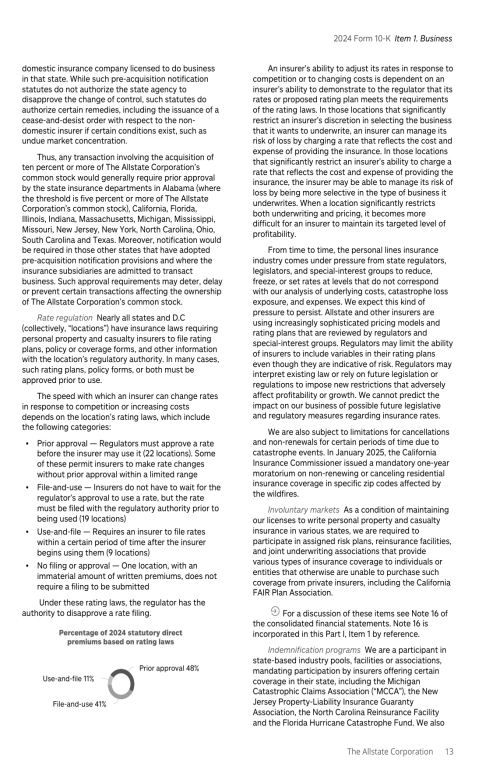

Regulation

Human Capital

Website

Other Information About Allstate

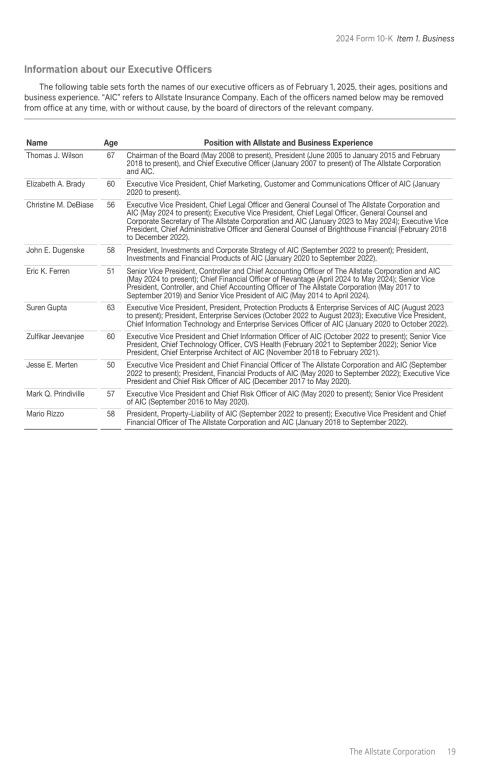

Information about our Executive Officers

Forward-Looking Statements

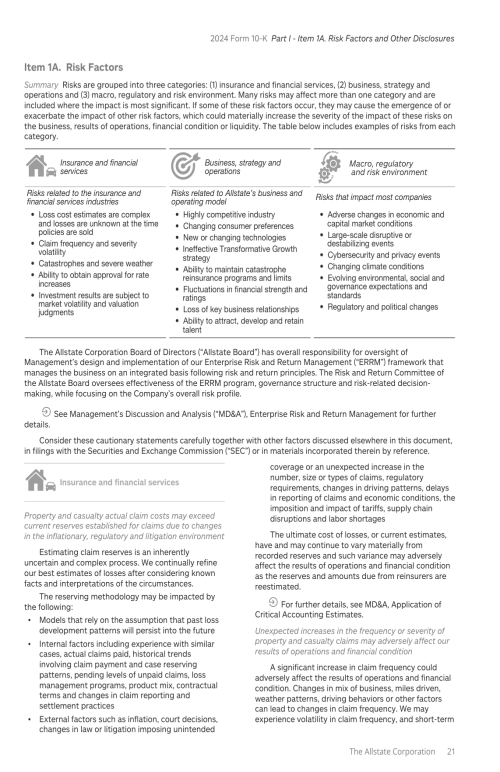

Item 1A. Risk Factors

Item 1B. Unresolved Staff Comments

Item 1C. Cybersecurity

Item 2. Properties

Item 3. Legal Proceedings

Item 4. Mine Safety Disclosures

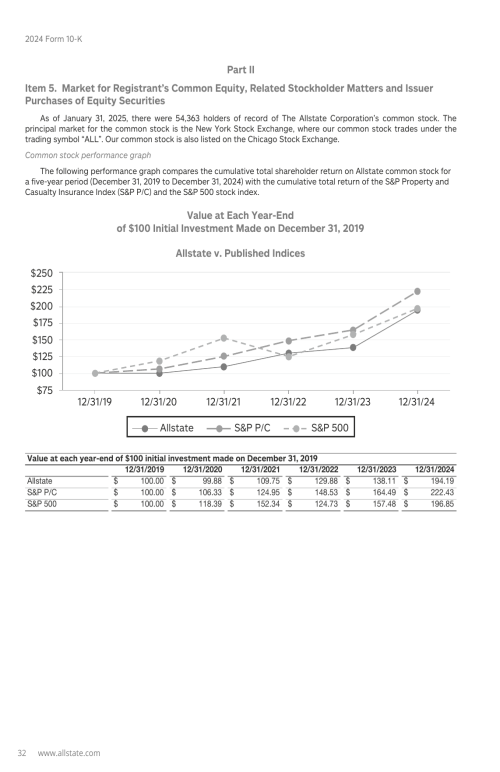

Item 5. Market for Registrant's Common Equity, Related Stockholders Matters and Issuer Purchases of Equity Securities

Item 6. [Reserved]

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Item 8. Financial Statements and Supplementary Data

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

Item 9A. Controls and Procedures

Item 9B. Other Information

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections

Item 10. Directors, Executive Officers and Corporate Governance

Item 11. Executive Compensation

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Item 13. Certain Relationships and Related Transactions, and Director Independence

Item 14. Principal Accounting Fees and Services

Item 15. Exhibits and Financial Statement Schedules

Item 16. Form 10-K Summary

Signatures

Financial Statement Schedules

Pages

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

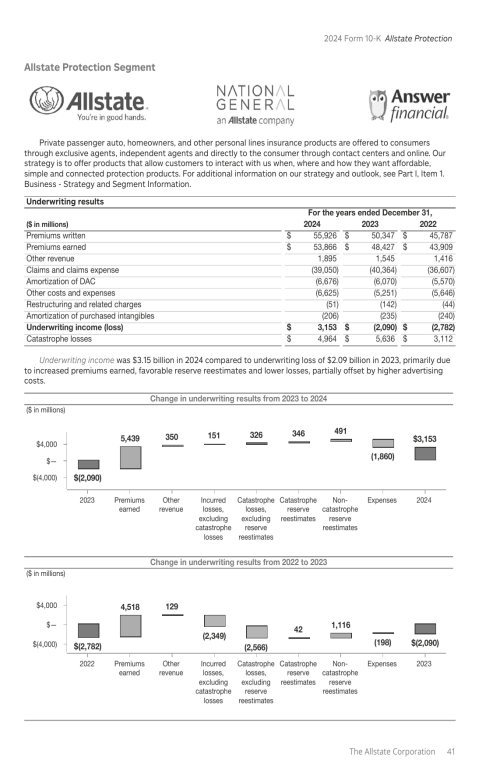

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

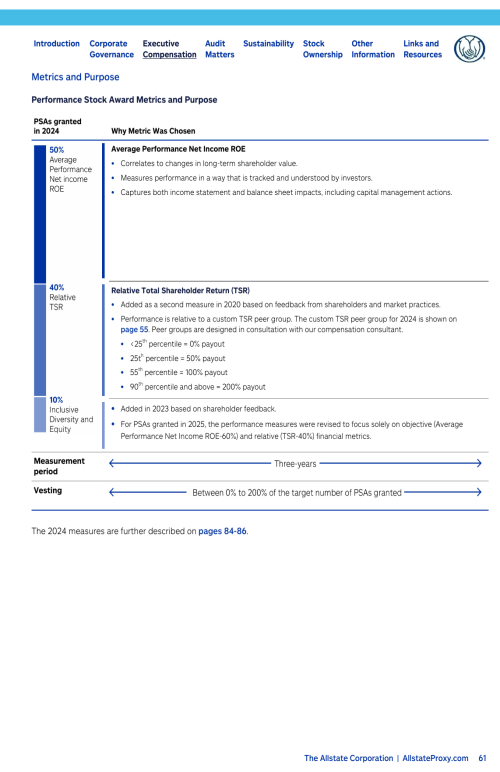

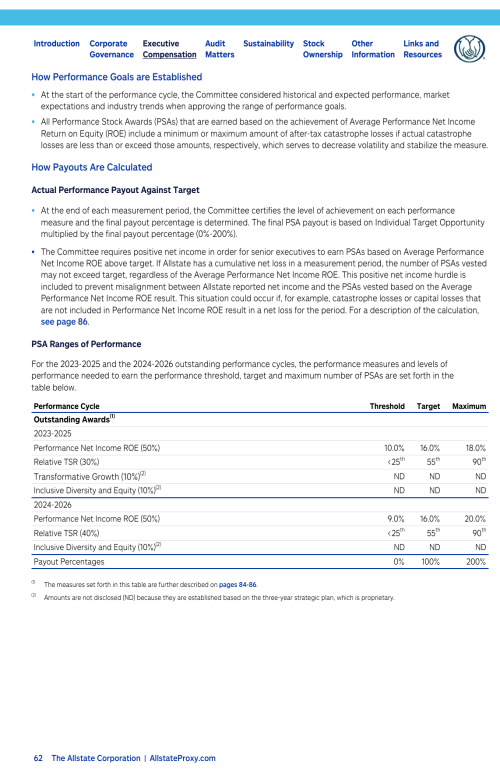

61

62

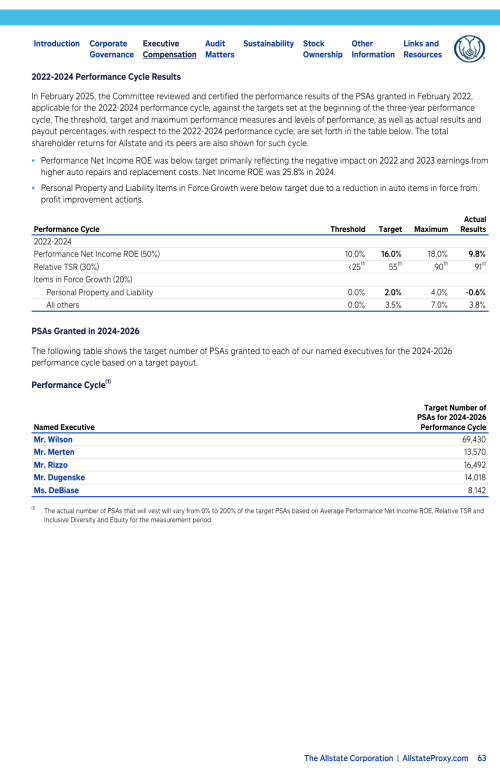

63

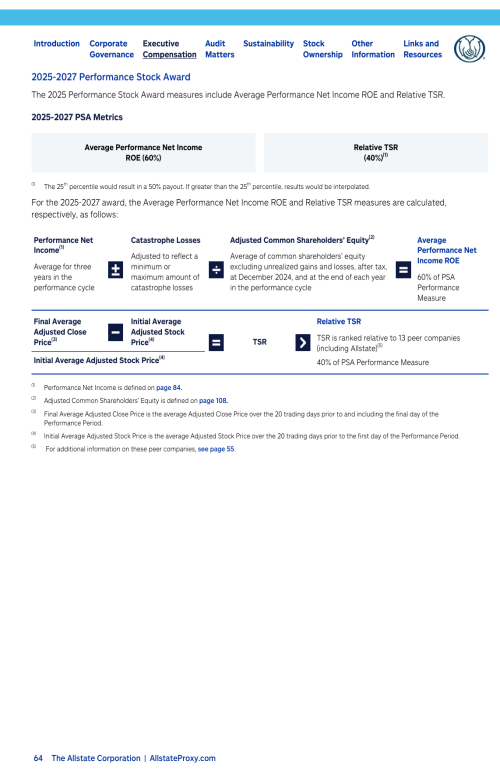

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

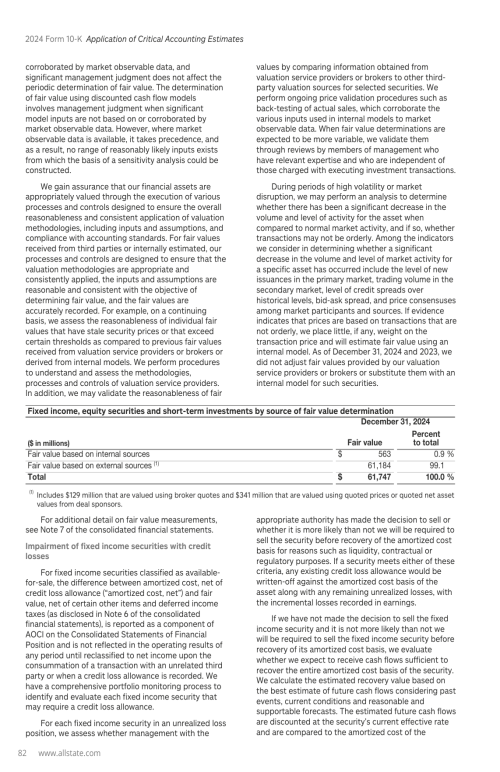

82

83

84

85

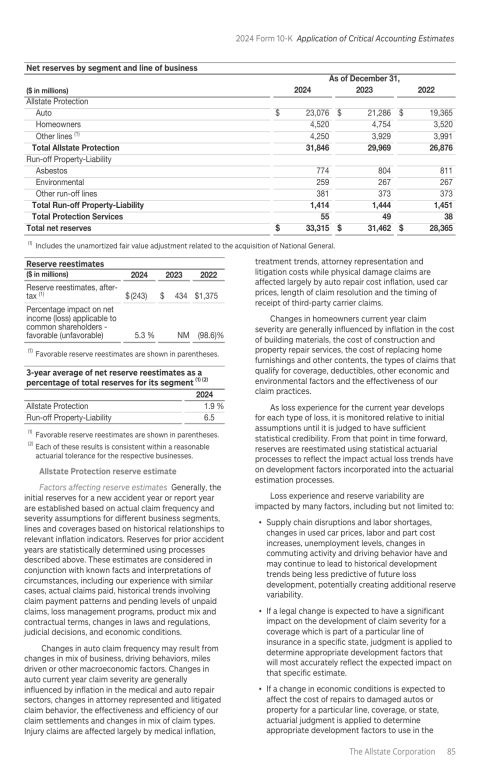

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

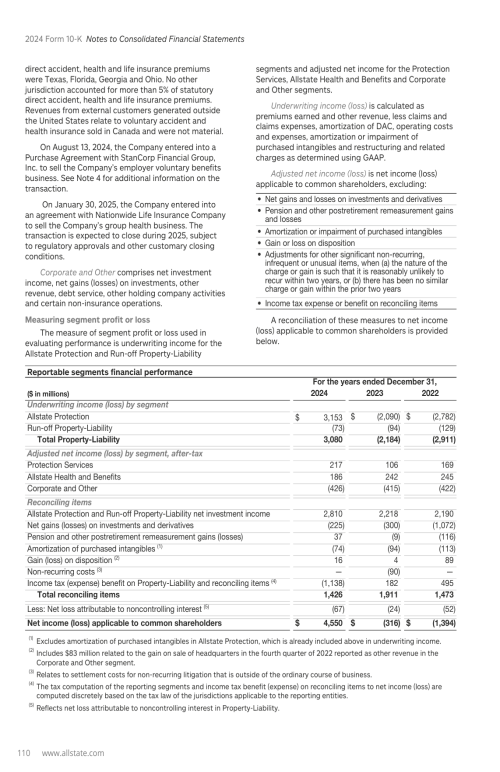

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157

158

159

160

161

162

163

164

165

166

167

168

169

170

171

172

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267

268

269

270

271

272

273

274

275

276

277

278

279

280

281

282

283

284

285

286

287

288

289

290

291

292

293

294

295

296

297

298

299

300

301

302

303

304

305

306

307

308

309

310

Search

Go to Home

Open index

Search

Index

Front Cover

Letter from Chair, President & CEO

Letter from Independent Directors

Notice of 2025 Annual Meeting of Shareholders

Table of Contents

About Allstate

Voting Roadmap

Corporate Governance

Proposal 1 Election of 13 Directors

Our Director Nominees

Corporate Governance Highlights

Board Composition and Nomination Process

Evaluating Board Effectiveness

Director Onboarding and Continuing Education

The Board and its Committees

Management Succession Planning

Risk and Return Management Oversight

Director Compensation

Executive Compensation

Proposal 2 Say-on-Pay: Advisory Vote on the Compensation of the Named Executives

Compensation Discussion and Analysis

Compensation Committee Report

Summary Compensation Table

Grants of Plan-Based Awards at Fiscal Year-end 2024

Outstanding Equity Awards at Fiscal Year-end 2024

Option Exercises and Stock Vested During 2024

Retirement Benefits

Non-Qualified Deferred Compensation at Fiscal Year-end 2024

Potential Payments as a Result of Termination or Change in Control (CIC)

Estimate of Potential Payments Upon Termination

CEO Pay Ratio

Pay Versus Performance Table

Audit Committee Matters

Proposal 3 Ratification of Deloitte & Touche LLP as the Independent Registered Public Accountant for 2025

Auditor Fees

Audit Committee Report

Sustainability at Allstate

Increasing Value for Customers and Shareholders

Navigating Climate Risk

Creating Opportunity for Employees

Improving Communities

Oversight of Sustainability

Stock Ownership Information

Proxy and Voting Information

Appendix A – Definitions of Non-GAAP Measures

Appendix B – Categorical Standards of Independence

Appendix C – Executive Officers

Helpful Links and Resources

Table of Contents 10K

Item 1. Business

Overview

Strategy and Segment Information

Regulation

Human Capital

Website

Other Information About Allstate

Information about our Executive Officers

Forward-Looking Statements

Item 1A. Risk Factors

Item 1B. Unresolved Staff Comments

Item 1C. Cybersecurity

Item 2. Properties

Item 3. Legal Proceedings

Item 4. Mine Safety Disclosures

Item 5. Market for Registrant's Common Equity, Related Stockholders Matters and Issuer Purchases of Equity Securities

Item 6. [Reserved]

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

Item 8. Financial Statements and Supplementary Data

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

Item 9A. Controls and Procedures

Item 9B. Other Information

Item 9C. Disclosure Regarding Foreign Jurisdictions that Prevent Inspections

Item 10. Directors, Executive Officers and Corporate Governance

Item 11. Executive Compensation

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

Item 13. Certain Relationships and Related Transactions, and Director Independence

Item 14. Principal Accounting Fees and Services

Item 15. Exhibits and Financial Statement Schedules

Item 16. Form 10-K Summary

Signatures

Financial Statement Schedules

Search